Brand and digital marketing

Business Strategy

Customer Strategy

Data analytics and insights

From Share of Search to Share of Model: What Portforlio Companies Need to Act On Now

March 30 2026

SEO isn’t dead. But the buyer journey it supports is getting rewritten by AI, quietly and fast. For PE-backed companies, the real risk isn’t that search vanishes. It’s that competitors start winning inside AI-driven journeys before anyone even thinks to open a browser.

In the recent LBO France Digital Forum, we answered some pressing questions.

Singulier conducts GEO and GEA workshop at the LBO France Digital Forum, March 2026

How are consumers finding brands now?

Generative AI has added a new, answer‑first interface on top of classic search. Prospective customers now move fluidly between:

- AI chats for ideas, shortlists and comparisons

- Traditional search for deeper research and validation

- Owned websites and sales touchpoints for evaluation and conversion

In other words, the buyer journey has become multi‑surface. Discovery and early consideration increasingly occur inside AI assistants; evaluation, pricing checks and transactions still depend heavily on web search and well‑structured sites.

For portfolio companies, this creates a new question: not “Is SEO still important?” (it absolutely is), but “Where along this blended journey are we invisible?”

Is SEO really dead now?

There is a temptation to frame GEO (Generative Engine Optimisation) as the successor to SEO. That’s the wrong mental model.

Search engines and AI models still rely on:

- Clean technical foundations: crawlable sites, fast load times, clear information architecture

- High‑quality content: genuinely useful, expert material mapped to real buyer questions

- Authority signals: links, mentions and engagement that validate expertise

These are classic SEO disciplines. They continue to drive a large share of qualified traffic and revenue in most sectors. Just as importantly, they influence which pages AI systems pull into their own answers. If your site is weak from an SEO perspective, you are unlikely to be trusted or cited by AI—no matter how “GEO-focused” your strategy claims to be.

SEO and GEO aren’t rivals. GEO only works if SEO has already done its job.

What happens if we don’t prioritise GEO?

What is changing is where competition shows up.

Historically, brands have fought for Share of Search: rankings, impressions and clicks in SERPs. That doesn’t go away. But they now need to fight simultaneously for Share of Model: how often, how prominently and how positively they appear in AI answers.

This has several implications:

- Buyers ask AI for the “best X for Y” and get a tiny shortlist. If you’re not on it, you’re not just losing traffic. You’re missing the whole conversation.

- AI environments compress choice. Instead of a page of ten blue links, a user might see three recommended brands. The winners capture a disproportionate share of intent.

- Traffic composition shifts. AI‑filtered visitors tend to arrive later in the decision process. Raw session counts may fall, but average intent and conversion potential rise.

For PE investors, that compression matters. It concentrates upside for brands that are consistently surfaced and recommended, while increasing risk for those that are generic, poorly differentiated, or absent from AI results.

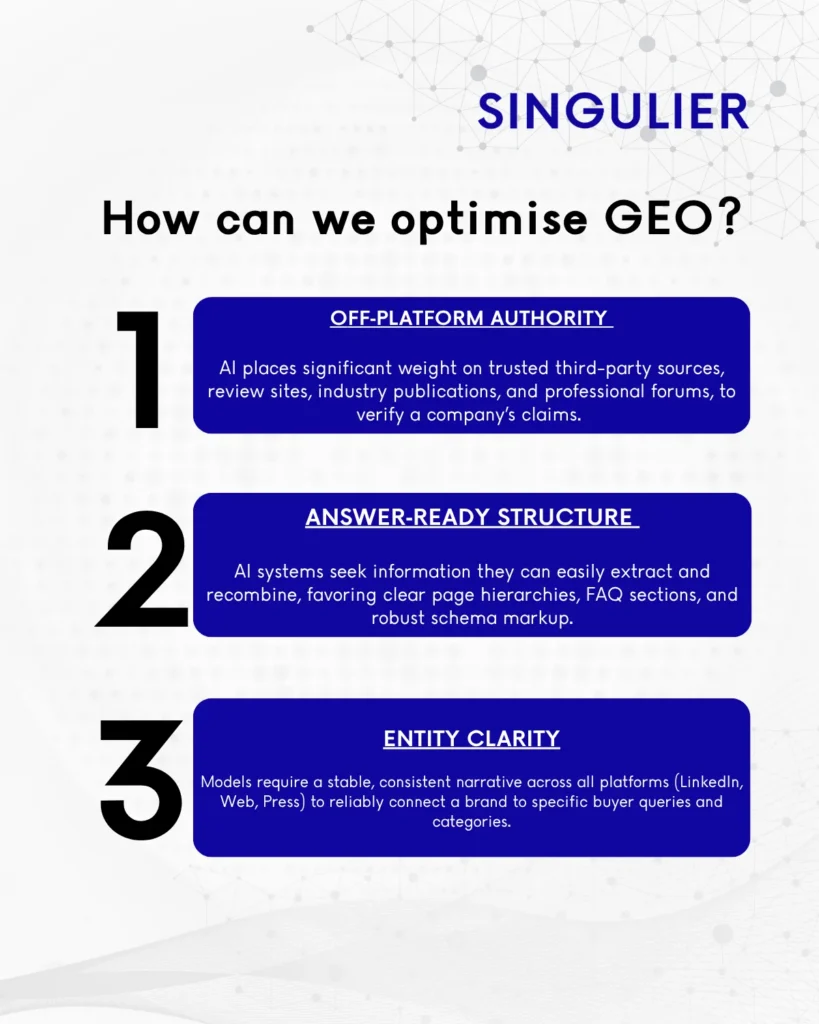

How can companies actually optimise GEO?

So what does it actually mean to “optimise for AI” without abandoning SEO fundamentals?

Three levers stand out.

1. Off‑platform authority

AI puts real weight on third-party sources it trusts: review sites, industry publications, marketplaces, professional communities, even forums.

For a mid‑market B2B SaaS platform, that might mean:

- Credible presence and reviews on G2/Capterra

- Thoughtful, expert contributions in niche communities

- Coverage in respected industry media rather than self distributed press releases

When AI sees a pattern—proof on your site, validation elsewhere—it’s more likely to put you on the shortlist.

2. Answer‑ready structure

AI systems look for information they can extract and recombine:

- Clear page structures with strong subheads and FAQs

- Schema markup that describes products, pricing models, locations and services

- Content written in plain language that mirrors how buyers actually ask questions

Many portfolio assets still bury their strongest proof points in dense copy, PDFs or unstructured case studies. That’s a problem for both search engines and AI. Being technically and structurally “readable” is now a matter of commercial hygiene.

3. Entity clarity

Models need to know who you are, what you do, for whom, and in which context. That sounds obvious, but inconsistent naming, muddled positioning and vague category language make it harder for AI to associate a brand with the right problem set.

A clear, stable narrative as mirrored in your website, LinkedIn, third‑party profiles and press coverage, helps models reliably connect your brand to the queries you care about.

What is GEA, and should we start investing in it?

If GEO is about earning your place in AI answers, GEA is about buying it.

As AI assistants become commercial surfaces in their own right, they are beginning to offer:

- Sponsored answers or highlighted recommendations alongside organic suggestions

- Conversational ad units (“Ask a follow‑up” that steers into a paid experience)

- Commerce integrations where users can research, compare and transact without ever hitting a traditional SERP

This introduces a paid layer on top of SEO and GEO. In high‑value, competitive categories, GEA can fill the gaps while GEO and SEO foundations are still maturing.

It allows brands to show up in crucial moments of buyer intent, even if they are not yet a default organic recommendation.

But effectiveness will depend heavily on the same ingredients: clarity of positioning, strength of value proposition, and the underlying authority signals that make a paid AI placement feel credible rather than intrusive.

Strategically, the move is not to shift budget blindly from search ads into GEA, but to treat GEA as an extension of performance marketing across a new interface: tested, benchmarked, and governed by the same ROI discipline as search, social and display.

What does this mean for PE-Backed Businesses?

For PE, the AI shift isn’t just a marketing sideshow. It’s a question of resilience.

- Revenue resilience: If a target or portfolio company relies heavily on organic search or aggregators, you need to understand how exposed those flows are to AI overviews and agents.

- Moats and differentiation: As models compress options, weakly differentiated propositions are more easily sidelined. Clear ICP focus and sharp positioning don’t just help humans, they help AI decide when you are the right answer.

- Exit narratives: Buyers are already asking how robust acquisition engines are in an AI‑first world. Demonstrating strength across both SEO and GEO can become part of a credible growth and risk‑mitigation story.

From Tactics to Discipline: What Leaders Should Do Now

Treat AI visibility as a strategic discipline, not a side project.

Three practical moves help management teams get ahead of the curve:

- Run an “AI & Search Reality Check”

Don’t debate AI in the abstract. Take 15–20 real buyer‑intent prompts and run them through the leading AI tools alongside conventional keyword checks. Note where your brand appears, how it is framed, who else is recommended, and where aggregators or marketplaces still dominate. This creates a concrete baseline for both SEO and GEO.

- Rebalance content toward “cite‑able” assets

Keep the SEO backbone: core landing pages, topic clusters, evergreen guides. But trim low‑yield, volume‑driven blogging in favour of assets that travel: expert commentary, data‑rich pieces, distinctive customer stories, and digital PR that earns genuine coverage and reviews. The aim is simple: give both humans and models more reasons to talk about you.

- Add AI brand health to the dashboard

If your operating reviews track rankings, organic sessions, CAC and LTV, they should now also track basic AI visibility and sentiment. Are you consistently present for critical prompts? Are you recommended or merely listed? Which competitors are gaining ground inside AI environments? You cannot manage what you never measure.

The GEO and GEA Opportunity for First Movers

The narrative around AI and search is often apocalyptic “SEO is dead” and “everything will be zero‑click.” That makes for good headlines but poor strategy.

A more useful lens is this: the cost of inaction is rising faster than the cost of experimentation. It is entirely possible to keep SEO strong, preserve existing demand engines, and layer in GEO capabilities in a measured, value‑accretive way.

The ones who get how SEO and GEO work together across the buyer journey and start building for both won’t just protect their traffic. They’ll compound their share of attention in a world where being the right answer, in the right place, at the right time, is the new digital leverage.

Let’s Talk

About Mathieu Ferel

Co-founder and Partner, FR

Mathieu Ferel is a Co-founder & Partner at Singulier, advising private equity funds and their portfolio companies, with a focus on brand strategy, media, CRM, and digital transformation. With focus on the consumer sector and strong expertise in fashion, luxury, and beauty, he helps funds drive due diligence insights and scale digital growth post-acquisition.

About Singulier Insights

Singulier Global Marketing Team